What is a Bank Reconciliation Statement

Bank reconciliation is the process that ensures that a company’s recorded cash balances align with the funds in their bank accounts. A Bank Reconciliation Statement is a financial document that ensures that the cash balances recorded in the internal financial records align with the financial records presented in the bank statement. In effect, the reconciliation statement is a document that presents the comparison between the internal financial records of a company (e.g. General Ledger) and the bank’s records (e.g. Bank Statement). It typically outlines outstanding checks, deposits in transit, bank fees, errors, and any other differences between the two sets of records.

Looking out for a Reconciliation Software?

Check out Nanonets Reconciliation where you can easily integrate Nanonets with your existing tools to instantly match your books and identify discrepancies.

This article presents the importance of bank reconciliation statements and provides insights into the benefits of automation in the generation of bank reconciliation statements.

The Importance of Bank Reconciliation

Bank reconciliation is the process of comparing a company’s financial records with the transactions reflected in its bank statements. It is important in maintaining financial integrity transparency and health. Bank Reconciliation does the following.

- Ensures the accuracy of financial records: Bank reconciliation acts as a safeguard, ensuring that the numbers reflected in a company’s internal financial records match precisely with the transactions recorded by the bank. This is critical for maintaining the integrity of financial data and facilitating informed decision-making.

- Detects errors, omissions, and irregularities: By comparing each transaction in the bank statement with the corresponding entry in the company’s records, bank reconciliation can catch discrepancies, errors, and omissions that may have occurred during the recording or transmission of financial data. Detecting and rectifying these discrepancies helps prevent inaccuracies from snowballing into significant financial misstatements.

- Safeguards against fraud and unauthorized activities: Bank reconciliation serves as a frontline defense against fraudulent activities such as unauthorized withdrawals, embezzlement, or check tampering. Discrepancies uncovered during the reconciliation process can raise red flags, prompting further investigation and measures to prevent financial losses and uphold the organization’s security protocols.

- Demonstrates commitment to financial integrity and regulatory compliance: Regular and accurate bank reconciliation reflects a company’s dedication to maintaining high standards of financial transparency and compliance with regulatory requirements. By reconciling bank accounts diligently, organizations can demonstrate their adherence to internal controls and external regulations, fostering trust among stakeholders and regulatory authorities.

- Instills confidence among stakeholders: Transparent and reliable financial reporting, supported by robust bank reconciliation practices, instills confidence among stakeholders, including investors, creditors, and business partners. Assurance of accurate financial data enhances credibility and fosters stronger relationships, facilitating access to capital, favorable credit terms, and business opportunities.

- Provides a solid foundation for sustainable growth and success: Effective bank reconciliation not only ensures the accuracy of current financial data but also lays the groundwork for future growth and success. By maintaining clean and up-to-date financial records, organizations can make informed strategic decisions, mitigate financial risks, and position themselves for sustainable growth and profitability in the long term.

What is a Bank Reconciliation Statement

A Bank Reconciliation Statement is the record of the comparison between the transactions recorded in the internal financial documents of a company and those in the bank statement. It serves as a tool to ensure the accuracy and integrity of financial data by identifying any differences between the two sets of records.

Typically, a Bank Reconciliation Statement contains the following components:

- Opening Balance: This is the balance of the company’s bank account at the beginning of the reconciliation period, as per the bank statement.

- Transactions: The statement lists all transactions that have affected the bank account during the reconciliation period. This includes deposits, withdrawals, checks issued, electronic transfers, bank fees, interest earned, and any other relevant transactions.

- Adjusted Bank Balance: This is the balance calculated by adjusting the opening balance with the total of all transactions listed in the bank statement.

- Internal Records: The company’s internal financial records are compared against the transactions listed in the bank statement. This includes accounting entries made for deposits, withdrawals, checks issued, and any other relevant transactions during the reconciliation period.

- Adjusted Internal Balance: Like the adjusted bank balance, this is the balance calculated by adjusting the opening balance with the total of all internal transactions recorded by the company.

- Reconciling Items: Any differences between the adjusted bank balance and the adjusted internal balance are listed as reconciling items. These may include outstanding checks, deposits in transit, bank errors, timing differences, and any other discrepancies that need to be addressed.

- Reconciled Balance: Finally, the reconciled balance is determined by adding or deducting the reconciling items from the adjusted bank balance. This represents the true balance of the company’s bank account after considering all reconciling factors.

How to prepare a Bank Reconciliation Statement

Preparing a bank reconciliation statement is a meticulous process that ensures the alignment of a company’s financial records with those of its bank. Here’s a step-by-step guide on how to prepare a bank reconciliation statement:

- Gather Bank Records: Obtain a comprehensive list of transactions from your bank. This can be acquired through bank statements or online banking portals. If your business operates multiple accounts, ensure you collect statements for each account.

- Compile Business Records: Open your ledger containing records of income and expenses. Whether it’s maintained in a logbook, spreadsheet, or accounting software, ensure all financial transactions are accounted for.

- Determine Starting Point: Identify the most recent instance where the balance in your business records matched that of your bank account. This serves as the starting point for the reconciliation process.

- Review Bank Deposits: Verify that each deposit recorded by the bank appears as income in your business records. If any deposits are missing, investigate the source, whether it’s from a sale, interest, refund, or other transactions, and ensure it is accurately recorded.

- Verify Income Entries: Cross-reference each income entry in your business records with corresponding deposits on your bank statement. Investigate discrepancies to ensure no income sources are overlooked or misrecorded, such as bounced customer payments.

- Examine Bank Withdrawals: Account for all bank withdrawals, including fees, in your business records. This step ensures that every expense is reflected in your financial records, even those that may have been initially omitted, such as bank fees.

- Confirm Expense Entries: Match each expense entry in your business records with withdrawals on your bank statement. Investigate any disparities, such as uncleared payments or transactions made using alternative methods, to reconcile the accounts accurately.

- Calculate End Balance: After carefully comparing all deposits and withdrawals, ensure that the final balance in your business bank account matches the total balances in your business records. This reconciled balance serves as the starting point for the next reconciliation process.

Reconciliation statement mismatches are common and manageable. Sources include timing differences, data entry errors, bank fees, outstanding deposits or checks, reconciliation errors, unrecorded transactions, errors in bank statements, and fraudulent activities. Timing discrepancies arise when transactions appear differently in bank and company records, while data entry errors occur during transaction recording. Bank charges may be inaccurately recorded, and outstanding deposits or checks can cause differences. Reconciliation errors, unrecorded transactions, and bank statement errors also contribute. Fraudulent activities, such as unauthorized withdrawals or forged checks, can lead to discrepancies and must be promptly addressed.

Importance of Automation in Generating Bank Reconciliation Statements

As a company grows and the number of transactions increases, manual bank reconciliation becomes inefficient. Here are some of the reasons why manual bank reconciliation is not a good idea:

- Time-consuming: Manual reconciliation involves matching each transaction in the bank statement with corresponding entries in the company’s records manually. This process can be extremely time-consuming, especially for businesses with a high volume of transactions.

- Prone to Errors: Human error is inevitable when reconciling transactions manually. Mistakes in data entry or calculation can lead to discrepancies in the reconciliation process, potentially resulting in inaccurate financial records.

- Limited Scalability: As businesses grow and transaction volumes increase, manual reconciliation becomes increasingly impractical. The time and effort required to reconcile larger volumes of transactions manually can become overwhelming and unsustainable.

- Difficulty in Tracking Changes: Manual reconciliation makes it challenging to track changes and updates in bank transactions efficiently. Any modifications or corrections made to transactions require meticulous manual adjustments, increasing the likelihood of errors.

- Lack of Real-time Insights: Manual reconciliation typically occurs periodically, such as monthly or quarterly. This means that businesses may not have real-time visibility into their financial position, leading to delayed decision-making and potential missed opportunities.

- Risk of Fraud: Manual reconciliation processes are more susceptible to fraudulent activities, such as unauthorized transactions or manipulation of records. Without automated checks and balances, fraudulent activities may go unnoticed for extended periods.

- Auditing Challenges: Manual reconciliation can pose challenges during audits or financial reviews. Auditors may have difficulty verifying the accuracy and completeness of manual reconciliations, potentially leading to audit findings or discrepancies.

- Opportunity Cost: The time and resources spent on manual reconciliation could be better utilized for more strategic activities, such as financial analysis, forecasting, or business development initiatives.

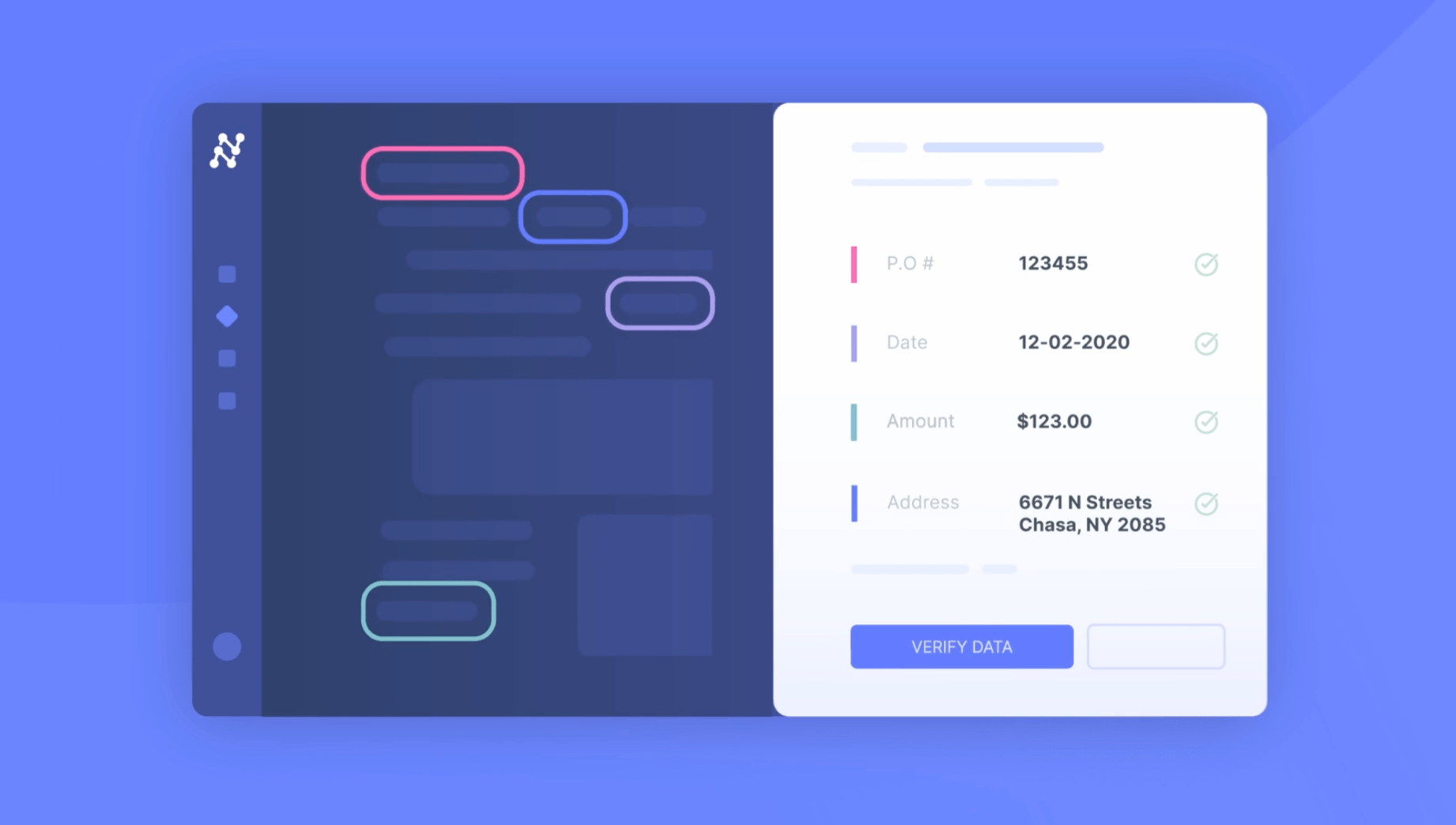

Nanonets for Bank Reconciliation Statements

Automation tools like Nanonets can help simplify the generation of bank reconciliation statements, making the process more efficient and accurate. With Nanonets, businesses can automate data extraction from bank statements, credit card statements, and invoices, saving significant time and effort. The platform’s advanced AI engine ensures precise data extraction without the need for predefined templates, enhancing accuracy. Some specific features of Nanonets that make it an ideal choice for bank reconciliation include:

Looking out for a Reconciliation Software?

Check out Nanonets Reconciliation where you can easily integrate Nanonets with your existing tools to instantly match your books and identify discrepancies.

- Automated data extraction from bank statements, credit card statements, and invoices

- Advanced AI engine ensures precise data extraction without predefined templates

- Flexible configuration options tailored to specific business rules and needs

- Seamless integration with existing tools for consolidated finance processes

- Enhanced accuracy in the reconciliation processes

- Real-time fraud detection capabilities, flagging duplicates, missing payments, outliers, or unauthorized transactions

- No-code blocks for in-app reconciliation and verification, eliminating the need for complex Excel sheets and multiple accounting tools

- Export data directly to CRM, WMS, or database, or choose from multiple file formats for offline use

- Ready-to-use solutions for common reconciliation use cases, customizable to match unique workflows and reporting needs.

Take Away

Bank reconciliation statements are essential for maintaining financial integrity and transparency in businesses. They ensure accuracy, detect errors and irregularities, safeguard against fraud, and enable regulatory compliance. Automated tools like Nanonets simplify the generation of reconciliation statements, offering features such as automated data extraction, advanced AI capabilities, flexible configuration options, seamless integration with existing tools, enhanced accuracy, real-time fraud detection, and customizable solutions. By leveraging automation, businesses can streamline their reconciliation processes, save time and effort, and ensure the accuracy and reliability of their financial data, facilitating informed decision-making and sustainable growth.