What Is a Bank Reconciliation Statement?

A bank reconciliation statement is a financial document that compares a company”s bank account balance to the transactions recorded on its general ledger, often called the “cash books.” The purpose of performing the bank reconciliation is to identify discrepancies and adjust entries so that the transactions are aligned with each other. They ensure the financial accuracy of the statements and are an essential process for the accounting teams involved in cash flow management.

How to perform a Bank Reconciliation?

Here are the steps involved in performing bank reconciliation.

Step #1

Collect your bank statement for the current period and compare it to your bookkeeping records or your company’s cash account records from the accounting system. The cash balance reported against both records might be different. We need to identify why these differences exist and make adjustments accordingly.

Step #2

Identify items that match both records. We can single out the unreconciled transactions by eliminating the entries that can be traced on both records.

Step #3

Identify items that have hit the company records but are missed on the bank statement. Cash that has been received and recorded by the company but has not yet been recorded on the bank statement is called “deposits in transit.” We need to add these to the bank statement.

“Outstanding Checks” are checks issued by the company but haven’t yet been cleared by the bank, meaning the funds have not yet been deducted from the company’s bank account balance. We need to deduct these from the bank statement.

Step #4

Now, look for items that are reflected on the bank statement but do not show up on the company’s bookkeeping records. These are generally issues like bank service fees, where banks deduct charges for services rendered, or bank errors and other issues. We need to deduct these charges from the accounting records.

Identify any interest earned by the company. These will be added to the accounting records.

Step #5

After adjusting both records, the bank statement balance should equal the adjusted cash record balance. Record the reconciliation by categorizing each discrepancy into one of the above types identified in steps 3 and 4 and grouping each category by aggregate values. Basically, you’re recording a change to the cash accounts in your general ledger.

After noting the discrepancies flagged by the general ledger and the bank statement, note how the bank account balance changes over the next few days. Ascertain the impact and note any unnoticed entries that hit the bank account.

Reconciliations are performed at the end of the month, with businesses with more transactions performing the process more frequently. Regular bank reconciliation is a key internal control measure that measures the accuracy of the company’s cash records and identifies any issues and discrepancies in a timely fashion.

Bank Reconciliation Example

Imagine you are working for a company, ABC, in the retail industry. You need to perform bank reconciliation at the end of the month (which can be daunting). Still, if you take the steps listed in the bank reconciliation example, you can ensure the financial accuracy of the records.

Record the balances registered for the bank account balance and the company’s cash account.

- Bank Statement Balance at the end of June 2024: $15,000

- Company’s Cash Account Balance in Records: $14,500

The company’s bank statement shows $15,000, but the company’s records show $14,500. This discrepancy needs to be resolved.

Step 1: Compare Bank Statement and Company Records

| Bank Statement | Company Records |

|---|---|

| $15,000 | $14,500 |

Items that match both records are highlighted. For example, a deposit of $5,000 on June 1st and a check #123 for $1,000 on June 3rd.

Step 2: Identify Matching Items

| Date | Description | Bank Statement Amount | Company Records Amount |

|---|---|---|---|

| 01/06/2024 | Deposit | $5,000 | $5,000 |

| 03/06/2024 | Check #123 | -$1,000 | -$1,000 |

Items like the deposit in transit and outstanding checks are identified. These need to be adjusted in the bank statement.

Step 3: Identify Items in Company Records but Not in Bank Statement

| Date | Description | Amount | Action |

|---|---|---|---|

| 04/06/2024 | Deposit in Transit | $1,500 | Add to Bank Statement |

| 05/06/2024 | Outstanding Check #124 | -$500 | Deduct from Bank Statement |

Items like bank service fees and interest earned are identified. These need to be adjusted in the company’s records.

Step 4: Identify Items in Bank Statement but Not in Company Records

| Date | Description | Amount | Action |

|---|---|---|---|

| 06/06/2024 | Bank Service Fee | -$50 | Deduct from Company Records |

| 07/06/2024 | Interest Earned | $25 | Add to Company Records |

After adjustments, the bank statement and company records should be reconciled and match.

Step 5: Adjusted Balances

| Category | Amount |

|---|---|

| Adjusted Bank Statement Balance | $16,000 |

| Adjusted Company Records Balance | $16,000 |

By following these steps and using the provided tables, Company ABC can accurately perform a bank reconciliation, ensuring its records are up-to-date and reflect the true financial status. Regular reconciliation helps identify discrepancies, prevent fraud, and ensure financial accuracy.

Why is Bank Reconciliation Important ?

Bank reconciliation is important for businesses for several reasons:

Error Detection:

Bank reconciliation helps identify errors in a company’s financial records. Issues like duplicate payments, missed payments, or incorrect transaction amounts can cause these errors. This ensures that customer payments have been made, which is critical when running a successful business.

Fraud Detection:

After closely scrutinizing both records, reconciliation can reveal unauthorized transactions and fraudulent activity. This allows businesses to take proactive measures, stop fraud, and recover any lost funds immediately.

Insights into cash flow:

With timely reconciliations in place, business can spot problems with cash flow by noticing how the inflows and outflows of cash are changing with time. This helps with cash flow management and better forecasting of the businesses’ finances.

Accurate Financial Reporting:

By guaranteeing the integrity of the company’s balance sheets, income statements, and other financial documents through regular reconciliations, businesses can help rely on the data and make informed business decisions.

Audit Compliance protocols:

Properly reconciled bank statements are required for accurate tax reporting and can help avoid penalties or issues during audits.

In summary, regular and thorough bank reconciliations are essential for businesses to detect errors, prevent fraud, manage cash flow, ensure accurate financial reporting, comply with tax requirements, and strengthen internal controls. It is a critical component of sound financial management.

Challenges faced With Bank Reconciliations

Businesses can gain many advantages by ensuring their accounting process’s financial integrity through regular bank reconciliations. Bank reconciliations help businesses detect expected payments that haven’t been made yet, detect fraud, and properly manage cash flow.

However the nature of bank reconciliation is extremely manual. Accounting teams can encounter multiple erros and inconsistencies dirung the manual comparision between the general ledger and the bank statement. Human made errors, managing multiple currencies and complex relationships between disaparte data sources can lead to excess time being consumed and error prone financial reporting;.

Lets list down some of the common mismatches that accountants come across while trying to do manual bank reconciliation:

“Outstanding Checks”:

These are payments that the company has sent out and recorded but has not yet cleared via the bank. Similarly checks that have been recieved by the business but haven’t yet hit the account have to be adjusted accordingly.

“Cash-In Transit”:

The cash might not immediately reflect in the bank account when funds are transferred via credit card payments or wire transfers. We need to make the proper adjustments here as well.

“Bank interest and service fees“:

Banks deduct charges for services rendered (typically relatively small), but they must be adjusted accordingly for accurate reconciliation. Similarly, banks pay interest in bank accounts, which must be accommodated accordingly.

“Obtaining necessary data“:

Managing high volume of transactions can be daunting and problematic due to disparate data sources that need to be identified and consolidated during the reconciliation process. Once an invoice is received we need to check whether the said goods have arrived against the relevant purchase order. Once confirmed, there needs to be an entry in the accounting system which needs to be reconciled against the purchase receipt. To consolidate all these paper receipts and no one place for digitising and a central database to list, it can be very time consuming to do the process against each entry in the accounting system.

“Numerous bank accounts and currencies”:

Companies often use multiple banks and accounts in different currencies. Reconciling transactions across these various accounts and currencies adds complexity to the process.

Manage Bank Reconciliations With Nanonets

Using Nanonets for your bank reconciliation tasks can help streamline the process by eliminating time-consuming, error-prone, and resource-intensive tasks when done manually. Nanonets offers an automated reconciliation software solution to approach this essential task.

“Automated data extraction”:

Nanonets’ Pretrained OCR models are better than big data generative AI models for data extraction. Generative AI solutions are not trained on labeled data, whereas Nanonets AI is constantly being trained on annotated data to extract data with higher accuracy. Nanonets AI learns how to map input features (like the fields you want to extract) to the output labels (name, date, balance) to achieve higher accuracy and scale with higher volumes of transformation data with ease.

.png)

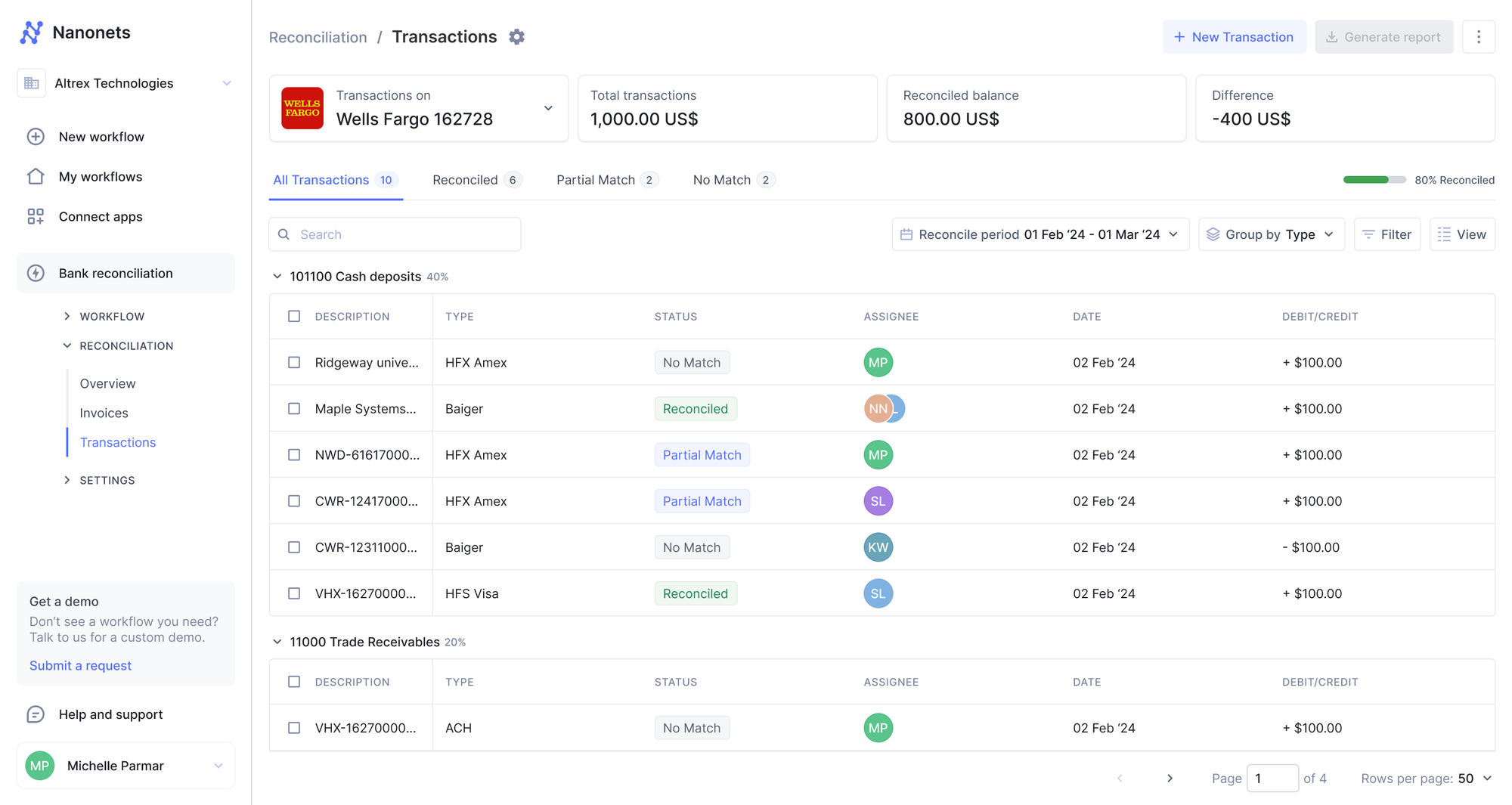

“Intelligent transaction matching”:

Nanonets AI leverages advanced algorithms, such as NLP techniques and fuzzy matching, to rapidly compare transactions between bank statements and accounting records. This reduces time taken for manual reconciliation from hours to just minutes.

“Centralised Data Repository“:

By consolidating all reconciliation data, supporting documents, approvals, and reporting into a single platform, Nanonets creates a comprehensive, auditable record of the bank reconciliation process. This centralized repository streamlines the reconciliation workflow, improves visibility, and enhances compliance.

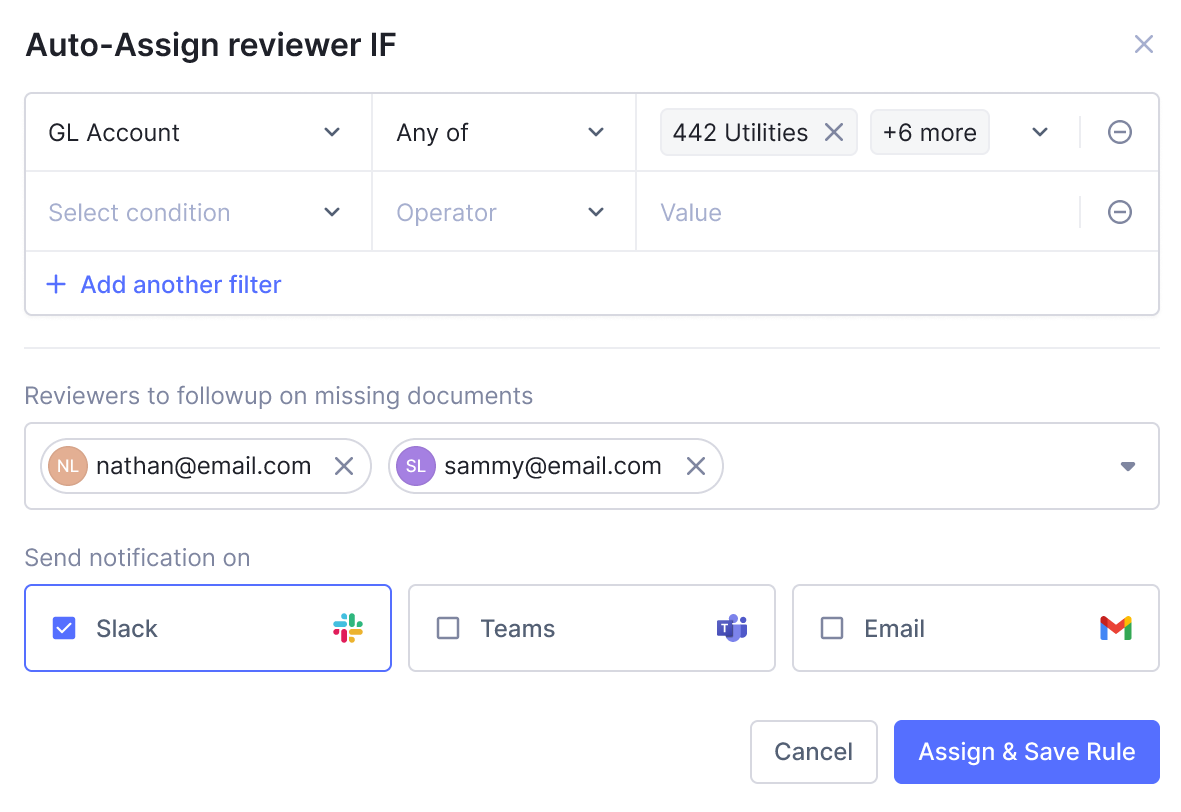

“Exception Management“:

Nanonets Reconciliation software can flag any unmatched and suspicious transactions, alerting the relevant members of the accounting team to investigate. Using Nanonets workflow automation capabilities, users can trigger and assign action items to the rest of the team for proactive resolution and achieve transparancy in the process.

“Scalability with high transaction volumes“:

Nanonets can handle high transaction volumens with speed and precision. Organizations trying to do manual reconciliation at the end of the month might need to hire more personals to deal with the high and fluctuating volumes of transactions. Nanonets frees up finance professionals to focus on more strategic tasks.

“Reporting and audit trails“:

Detailed reconciliation reports are generated automatically, providing a full process audit trail. This improves compliance and visibility.

.png)

By adopting Nanonets, businesses can save significant time and money, improve data accuracy, strengthen internal controls, and enhance overall financial management. It is a powerful tool for streamlining the critical bank reconciliation process.