As everyday tools and services become increasingly subscription-based, so too does our overall automation strategy when it comes to business management. But, just as keeping a subscription on automatic renewal without oversight can be a costly mistake, so too can mismanaging recurring ACH transactions.

QuickBooks, one of the most popular accounting and bookkeeping platforms on the market, offers a fairly straightforward method of managing recurring ACH payments to help ensure no surprises come during reconciliation time.

What are ACH Payments?

Though usually just called ACH payments or ACH transfers, the term more specifically refers to a national payment network that banks and other institutions rely upon to process payments securely and accurately between parties. In its simplest form, the ACH network is like a trusted third party that receives money from the payer and processes it on their behalf before depositing it into the payee’s account.

ACH payments are generally fast during the work week but aren’t instantaneous. Instead of directly routing to the payee upon payment, like payment apps and similar processing tools, the ACH network batches and routes payments daily rather than individually. This is why ACH payments generally take 1 – 3 business days to execute, though ACH payments are increasingly same-day when submitted during business hours early enough in the day.

ACH payments will generally fall under one of two primary categories:

Direct payment: This type of ACH payment describes how a buyer pays for goods or services. Examples include direct ACH payments for utility bills, to a friend as an alternative to wire transfers, and to your credit card company to pay your monthly statement.

Direct deposit: The variety of ACH payment we’re most familiar with, direct deposit refers to businesses, employers, and government entities offering ACH payments to recipients for payroll, government entitlements and benefits, and even tax refunds.

Within these two broad labels, depending on your role in the exchange, your transaction will be categorized as:

ACH Credit: If you’re on the receiving end, your account is credited the payment balance from the sender’s account. ACH credit transactions can include your payroll, government benefit payments, tax refunds, or invoiced payments for contractors.

ACH Debit: The sender’s transaction is an ACH debit, as the money is debited from their account when sent to the recipient. If you pay your mortgage via ACH payment, then it’s an ACH debit transaction.

What are Recurring ACH Payments?

Often, for predictable and ongoing expenses, we’ll set up recurring ACH payments to ease the mental burden and avoid the risk of missing a bill. Recurring payments occur on a programmed basis and debit the exact amount stated; they tend to be best for fixed costs like subscriptions, mortgage or lease payments, and membership costs. Payroll deductions, though variable, are also typically classified as recurring to reduce friction between payroll processing and getting staff paid.

Recurring vs. Automated ACH Payments

Though recurring payments are automated, not all automated payments are recurring. Whether an ACH payment is classified as recurring depends on frequency – if payment occurs on a planned schedule periodically, i.e., monthly, it’s recurring. If it’s a preplanned and preprogrammed ACH payment set to execute in the future but on a one-time basis, it’s simply an automated ACH payment.

How do Recurring ACH Payments Work in QuickBooks?

If you plan to use recurring ACH payments in QuickBooks, note that only QuickBooks Online offers the feature – as QuickBooks sunsets its Desktop platform, expect new integrations and features to be exclusive to the Online platform; recurring ACH payments are no exception.

Recurring Payments from Customers

Before receiving any ACH payment in QuickBooks, you must have an active QuickBooks Online and QuickBooks Payments license. Before getting started, you’ll also need client authorization to bill. Whether this is verbal or written consent, validating that your customer knows an ACH transaction is inbound is just good customer service.

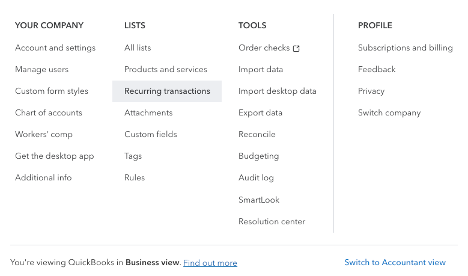

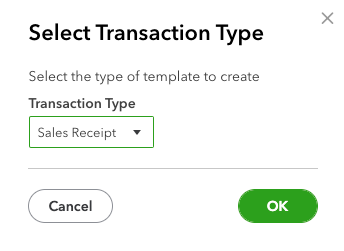

From there, you’ll:

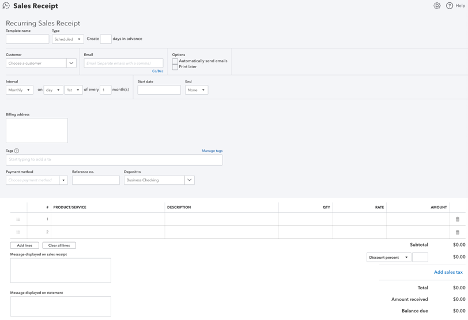

Add the recurring transactions by selecting Recurring Transactions from the settings dropdown menu.

Click New, then select Sales Receipt from the dropdown menu.

You’ll then fill out all customer or client information.

And that’s it! Beyond keeping an eye on the recurring ACH payments, validate one final time before pulling the trigger that your client or customer knows about and agrees with the recurring ACH payment; otherwise, you’re good to go!

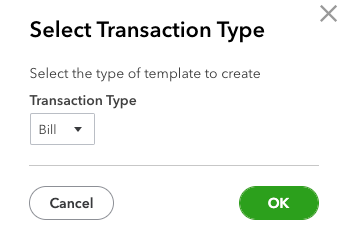

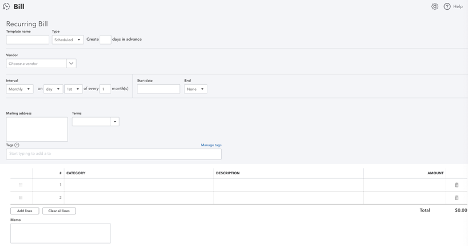

Payments to Vendors

You’ll follow the same steps as above, though instead of selecting Sales Receipt, you’ll click Bill:

From there, simply populate the vendor’s data or select an existing supplier and recurring payment interval – it’s that easy!

How to Stop Recurring ACH Payments in QuickBooks

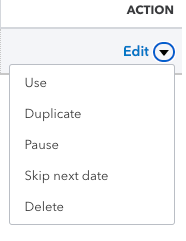

Once you have a recurring ACH payment set up in QuickBooks, whether credit or debit, you can monitor its status from the Recurring Transactions dashboard:

Cancelling or stopping a recurring ACH payment is as simple as selecting the Edit dropdown menu under the Action column and selecting Delete. You can also pause the recurring ACH payments or skip the next recurring ACH payment.

Disadvantages of Recurring Payments in QuickBooks

Though no system is perfect, establishing and using recurring payments in QuickBooks does come with some unique drawbacks:

- Daily limits: If you initiate the ACH (credit or debit) from an external bank, you’re restricted to a $500,000 daily deposit limit (into QuickBooks) and a $100,000 weekly debit limit (money sent out of QuickBooks). If you initiate the ACH transfer from QuickBooks, you can transfer up to $20,000 daily and $40,000 weekly into QuickBooks and up to $50,000 daily out of QuickBooks.

- Processing delays: Though the ACH network has gotten faster in recent years, there’s no guarantee that an ACH payment will fully execute the same day. That’s especially true if you initiate the transaction outside of standard business hours.

- Insufficient fund risk: Though not tied to QuickBooks specifically, you always run the risk of overdrawing accounts or paying insufficient fund fees if you fail to monitor your debited account balance. Again, not an inherent risk or drawback, but one that can be frustrating and costly.

- International payments: QuickBooks lacks native cross-border ACH payment integration; though third-party add-ons fill the gap, companies working extensively with international vendors or buyers may find better solutions elsewhere.

Alternatives to ACH Payments in QuickBooks

If you’d prefer not to use QuickBooks for ACH payments – or want to avoid ACH transactions altogether – plenty of alternatives give you flexibility to choose the systems that best align with your workflows. Some common alternatives include:

- QuickBooks GoPayment: For QuickBooks users, this mobile payment app serves as an alternative to ACH transactions and includes automatic synchronization with your primary account.

- Other apps: A range of mobile payment processing apps give on-the-go flexibility and ease of use, including Venmo, PayPal, and CashApp.

- Payment processors: If you need more robust transaction management tools, payment processors like Square and Stripe provide all-in-one payment solutions.

- Wire transfers: Though costlier in most cases, wire transfers are popular for international and cross-border transactions.

Conclusion

Though alternatives exist, managing recurring ACH transactions directly within the QuickBooks platform tends to be a safe bet for users interested in keeping their business accounting on a centralized platform without having to learn and manage multiple products. Recurring ACH transactions are a simple, safe, and easy way to keep cash coming in and vendors happy – and QuickBooks simplifies the process even further.