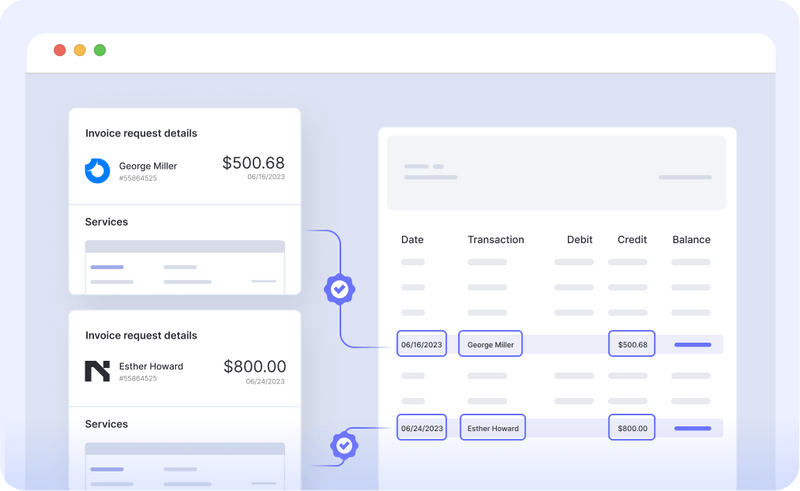

Bank reconciliation is the process of matching the company’s cash ledger with the bank statements. The objective is to scrutinize each transaction and identify any errors or potential fraud.

The two ledgers generally don’t match due to factors such as bank fees, interest, outstanding checks, and deposits in transit. These discrepancies must be accounted for in a bank reconciliation statement to represent the current financial position accurately.

In this blog, we will present some real-life examples of bank reconciliation statements and help solve the major problems faced during bank reconciliation.

What Is a Bank Reconciliation Statement?

A bank reconciliation statement is a financial document that compares the company’s cashbook with the bank statements to ensure accuracy and consistency in financial records. This process helps the company monitor and update its funds, addressing any discrepancies that may arise. If inconsistencies are identified, they must be rectified or appropriately explained.

The bank reconciliation process thoroughly investigates the causes of discrepancies between the two accounts. Several reasons contribute to such discrepancies:

- Bank Charges – Bank accounts can incur overdraft charges, account maintenance charges, or other penalties that might not have been marked in the company cashbook. Alternatively, any interest incurred on the bank balance has to be accounted for in the cashbook.

- Outstanding Checks – Checks issued to vendors might not be submitted but accounted for in the ledger. Bank processing delays could also result in checks not being reflected in the statement till the end of the recording period.

- Payment Delays: Payments made through ACH or Wire can take up to several days before hitting the bank. This can result in the transaction missing from the statement.

- Accounting/Banking Error: The bank or the company accountant could have made a mistake in accounting a transaction. Common examples – are missed payments, double payments, or refunds.

Common examples of bank reconciliation statements

Now let’s look at examples of real-life bank reconciliation statements and the type of issues you can face:

Bank Charges

XYZ Corp’s bank balance on December 31, 2023, is $10,000, whereas the cashbook balance is $10,300. The variance is attributed to specific bank charges. Let’s examine the transactions:

- A $200 penalty was incurred due to a bounced check, recorded in the bank statement but not in the cashbook.

- $300 was levied as the annual bank maintenance charge, recorded in the bank statement but not in the cashbook.

- A $100 dividend was disbursed from the stock portfolio, recorded in the bank statement but not in the cashbook.

- A $100 quarterly interest payment by the bank, recorded in the bank statement but not in the cashbook.

Outstanding Checks – Bank balance > Cashbook balance

XYZ Corp has a bank balance of $10,000 as of December 31, 2023, while the cashbook balance is $9,000. The lower cashbook balance is attributed to outstanding checks. Let’s examine the transactions:

- Two checks totaling $1,400 were issued but are yet to be processed. This transaction is recorded in the cashbook but not in the bank balance.

- An inbound payment of $400 from a client has been initiated but has not yet cleared the bank. This transaction is recorded in the cashbook but not in the bank balance.

- A $100 quarterly interest payment by the bank is documented in the bank statement but is not included in the cashbook.

Payment delays – Cashbook balance > Bank balance

XYZ Corp has a bank balance of $20,000 as of December 31, 2023. However, the cashbook balance is $18,000, reflecting a higher balance due to banking delays where certain transactions were not recorded by the cutoff date. These transactions were recorded on January 3, 2024. Let’s explore the details:

- Two checks totaling $4,000 were issued but have not been processed yet. These are marked in the cash book but not reflected in the bank balance.

- An inbound payment of $2,000 through ACH was processed four days after it was initiated. Although it was marked on December 31 in the cashbook, it appears in the bank statement on January 4.

Accounting Errors

XYZ Corp has a bank balance of $20,000 as of December 31, 2023. However, the cashbook balance is $15,000. Upon investigation, errors in recording payments by the accountant have been identified. Let’s examine the transactions:

- A $2,000 check was issued but was never recorded in the cashbook.

- A vendor payment of $500 was mistakenly recorded twice on separate dates despite being processed only once.

- An inbound payment of $500 was erroneously entered as $5,000.

- A transaction of $1,000 could not be processed and was subsequently refunded.

Banking errors

XYZ Corp has a bank balance of $10,000 as of 31st Dec 2023. However, the cashbook balance is $12,000. The bank balance is lower due to a few banking-related errors:

- The client’s payment of $1000 isn’t reflected as the client made a mistake with the account number.

- The Bank transaction failed, and the refund of $1000 hasn’t been processed.

- The Bank statement shows an error where an inbound $1000 transaction is accounted for as $3000.

- The bank lost or misplaced your check for $2000.

Banking errors can be disputed with the bank and resolved. Bank reconciliation is vital in discovering such errors timely within dispute windows!

Bank Reconciliation Alternative Format

In the above method, we accounted for various transactions that created discrepancies between the cashbook and bank balance. Alternatively, companies “adjust” the ledgers to prepare a bank statement. In this method:

Step 1: Adjust bank balance

Bank statements must be adjusted by adding pending deposits (deposit-in-transit) and deducting pending outgoing checks (outstanding checks). The logic here is:

Bank Balance + Deposits-in-transit – Outstanding Checks = Adjusted Bank Balance

Step 2: Adjust cashbooks

The cashbook balance needs adjustment for bank service fees, accrued interest, and rejected checks (NSF Checks). The logic here is:

Cashbook Balance + Interest – Bank Fees – Rejected Checks = Adjusted Cashbook

How to Streamline Bank Reconciliation?

Bank reconciliation is a tedious process with several manual steps. A more efficient approach is to adopt bank reconciliation software, which reduces manual errors and enhances organization and time savings through automation.

Bank reconciliation tools primarily employ two reconciliation methods: Document Review and Analytics Review. In Document Review, OCR-powered software extracts pertinent data from documents and presents it in the required format. Automation tools like Nanonets take it a step further, enabling users to define rules for detecting anomalies, duplicates, and mismatches. If the software can identify discrepancies, it significantly simplifies the reconciliation process by over 90%.

Automate your mortgage processing, underwriting, fraud detection, bank reconciliations or accounting processes with a ready-to-use custom workflow.

Nanonets simplifies and streamlines the account reconciliation process with its AI-powered workflow automation solution. This tool automates various steps, minimizing manual effort and boosting efficiency by a factor of 10.

If Nanonets aligns with your business requirements, feel free to ask for a customized quote tailored to your specific needs.