Bank Reconciliation is the process of matching the company’s cash balance to the bank statement. The aim is to ensure all transactions, like customer payments, bank fees, outstanding checks, and refunds, are accurately recorded in the company’s cashbooks.

Bank reconciliation is crucial for identifying accounting errors and detecting fraud or theft. Without proper reconciliation of statements, a company risks financial losses due to errors and fraud. Moreover, inaccuracies in the cashbooks can lead to complications in financial planning, tax compliance, and legal matters.

How does bank reconciliation work?

Bank reconciliation involves two strategies: a micro and a macro strategy. The first is document review, where each transaction is cross-checked and accounted for. The second is the analytics review, where we observe trends from previous years to conduct a sanity check on income/expenses and detect outliers. Accounts payable teams are expected to apply both methods during their reconciliation process.

- Documentation review

Document review entails comparing the cashbook and bank statement on a transactional level. It requires a comprehensive assessment of each transaction to detect any irregularities.

For instance, let’s say an accountant pays $500 to a vendor but forgets to write it down. Another person noticed the missing entry and paid the $500 again, and now the company has made double payments. However, only one payment is noted in the cashbook. While comparing the cashbook to the bank statement, the accountant can identify the duplicate payment and subsequently request a refund from either the vendor or the bank for the second payment. Similarly, you can detect banking errors like undue fees and incorrect transactions. In the next section, we will go into more detail on how to do a document review.

- Analytics review

The analytics review method looks at the bigger picture to identify changes in trends. During this analysis, estimations are formed based on historical account activity, serving as a benchmark for comparison with the cashbook records. Any unusual data is a starting point to uncover potential errors or fraud.

For instance, a company usually has a monthly vendor payment of $200K, but it’s recorded as $400K this month. Considering that the overall income hasn’t significantly changed, and previous payments from months and years don’t fall in this different range, it raises concerns. Upon investigation, the accountant found a payment of $20K mistakenly recorded as $200K.

Analytics review is an effective way to identify significant variations and outliers.

How to do bank reconciliation?

Bank reconciliation involves matching the money in the bank vs the actual money reflected in the cashbook. Today, reconciliation is primarily automated through reconciliation software to save time and money. However, let’s understand the manual bank reconciliation process once:

Step 1: Gather documents

On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. On the company side, you require the company’s cashbook, which records both incoming and outgoing transactions.

Step 2: Match deposits

Following double-entry accounting, a debit in the bank statement is recorded as a credit in the cashbook, and vice versa. Match the deposits in the two statements.

Note: Bank and cashbook balances are generally not expected to match due to pending transactions, such as outstanding checks or deposits in transit. They have to be adjusted as shown in the next steps.

Step 3: Adjust bank balance

The discrepancy in the two balances has to be identified and checked on an individual transaction basis. Bank statements must be adjusted by adding pending deposits (deposit-in-transit) and deducting pending outgoing checks (outstanding checks). The logic here is:

Bank Balance + Deposits-in-transit – Outstanding Checks = Adjusted Bank Balance

Step 4: Adjust cashbooks

The cashbook balance needs adjustment for bank service fees, accrued interest, and rejected checks (NSF Checks). The logic here is:

Cashbook Balance + Interest – Bank Fees – Rejected Checks = Adjusted Cashbook

Step 5: Compare Balance

After adjustment, the bank balance and cashbook should match. If they are not equal, there is an error in the reconciliation process. Any unwarranted expenses or missing income should be investigated and accounted for during the reconciliation process.

Why is it important to reconcile your bank statements?

It’s important to reconcile bank statements to identify errors, detect fraud, and maintain an accurate ledger. Here are the key benefits of bank reconciliation:

- Identify Accounting Errors: The cashbook may contain inaccuracies stemming from duplicate payments, missed payments, lost checks, and even simple human errors. Reconciliation is crucial in identifying and correcting these mistakes before they become permanent.

- Rectifying Banking Errors: The bank statement may contain errors like undue penalties or incorrect transaction records. If you identify any such errors, you can dispute and rectify them with your bank.

- Fraud Prevention: This stands out as a key benefit of bank reconciliation. When cross-referencing records, it becomes straightforward to pinpoint any transactions that were not supposed to occur. It’s plausible that either a team member or a hacker executed unauthorized transactions to steal from the company. Regular reconciliation helps catch and stop potential fraud early, giving the bank time to reverse transactions.

- Accurate Tax Reporting: Reconciliation helps form an accurate set of financial records on a timely basis. Filing tax returns requires an accurate record, or you can incur penalties. Regular Bank Reconciliation simplifies the tax reporting process during the financial year’s end.

- Financial Optimization: Identify and Save on unwarranted fees like overdrafts or penalties.

How Often Should You Perform a Bank Reconciliation?

The frequency of bank reconciliation depends on the volume and type of business. If you deal with a high transaction volume, it’s more efficient to reconcile frequently, avoiding a backlog of work.

- Monthly: Traditionally, companies conducted bank reconciliation monthly upon receiving a new bank statement. Monthly reconciliation is a widely accepted method.

- Daily: Online banking can generate statements anytime, allowing for daily reconciliation. Daily bank reconciliation offers the advantage of a more accurate cash flow estimate and quick fraud detection. It’s also easier to stay current with events by reconciling promptly rather than waiting months after an occurrence.

The only downside is that daily reconciliation takes time with a manual bank reconciliation process. However, this can be significantly streamlined with automated bank reconciliation.

How to Automate Bank Reconciliation

Bank reconciliation is a time-consuming process with many manual steps. Most automation tools provide OCR capability that extracts relevant information from documents. However, this is just one aspect of your workflow. You need a tool to build a customized workflow, automating business logic while integrating with existing tools.

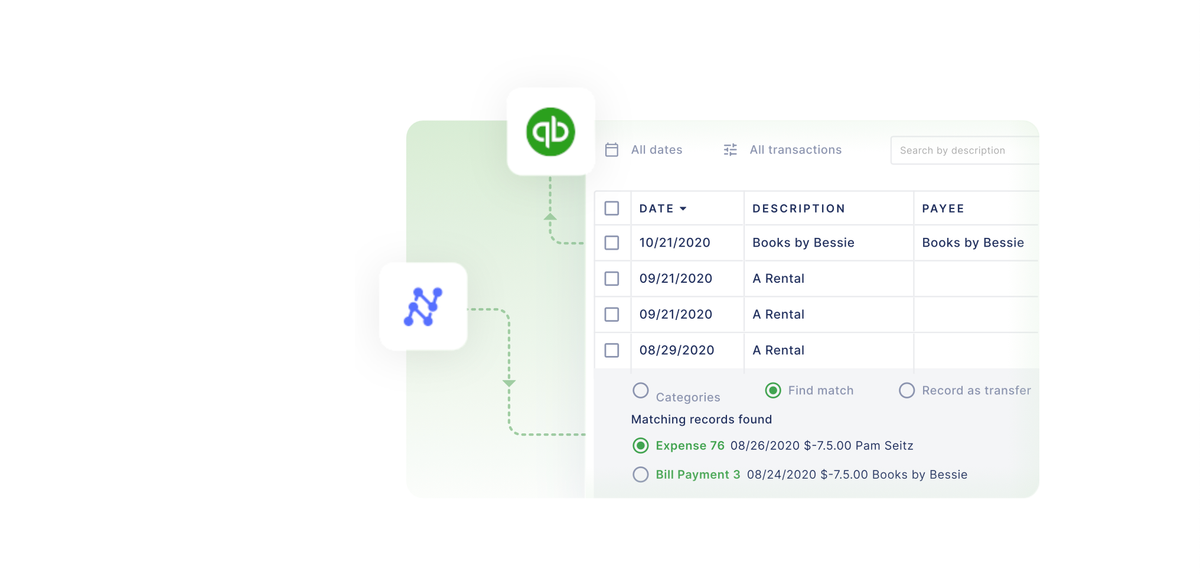

Nanonets is an AI-powered workflow automation solution that simplifies and streamlines account reconciliation. It automates various steps, reduces manual effort, and increases efficiency by 10x.

The Nanonets bank reconciliation workflow works like this:

- Automated import: Nanonets can automatically import documents like bank statements from mail or through the bank API.

- Data extraction: Nanonets uses state-of-the-art optical character recognition (OCR) technology to extract relevant data accurately. This eliminates the need for manual data entry, which can save time and reduce errors.

- Data matching: Nanonets allows you to set up a rule-based matching to identify and reconcile transactions across different systems. This helps ensure that all transactions are accounted for and there are no errors.

- Approval: Nanonets can automate the account reconciliation process, from data entry to approval. This can free up time for accountants to focus on other tasks.

- Centralized repository: Nanonets provides a central repository for supporting documentation. This makes it easy to find and access documents when needed.

If Nanonets meets your business requirements, you can get in touch for a customized quote.

Summary:

Ensuring the accuracy of financial records, detecting fraud, managing cash flow, complying with tax regulations, and meeting legal requirements are crucial for businesses of all sizes. Reconciling bank statements is a key practice in achieving these goals. There are two primary reconciliation methods: document review, which involves matching transactions, and analysis review, where comparisons are made to historical trends.

Regular reconciliation is essential for the early detection of fraud or errors. However, this process can be time-consuming. Streamlining it through automation software, such as Nanonets, is recommended to enhance efficiency.

FAQs

What are the 4 steps in the bank reconciliation?

Compare records: Match your internal financial records with the transactions listed on the bank statement to identify any discrepancies.

Adjust balances: Factor in any outstanding checks, deposits in transit, bank fees, and errors to adjust the balance of your financial records accordingly.

Journalize differences: Make the necessary journal entries for discrepancies between your records and the bank statement after adjustment.

Verify final totals: Review the adjusted book balance and the adjusted bank balance to ensure they are now reconciled and the same.

If there are differences, investigate and resolve them to ensure that the records are accurate, complete, and within the financial reporting framework.

How do you reconcile a bank statement?

To reconcile a bank statement, compare your internal ledger against the bank statement for the same period. Identify any mismatched transactions, such as deposits in transit and outstanding checks. Adjust for bank errors, fees, and interest. Make journal entries for these adjustments and review the final reconciled balance to confirm that the records align.

What is BRS in simple words?

Bank Reconciliation Statement (BRS) is a document that matches the cash balance on a company’s balance sheet to the corresponding amount on its bank statement, reconciling any differences to ensure that the figures are accurate and consistent. It serves as a check to verify that all transactions have been recorded correctly in the company’s and the bank’s records.

Is bank reconciliation debit or credit?

Bank reconciliation itself is neither a debit nor a credit. It is a process of comparing the balances and transactions in one’s accounting records against the bank statement to identify any discrepancies and make the necessary adjustments to the accounting records.

What are the steps to reconcile a bank statement?

Identify discrepancies:

Compare each transaction from your accounting records with those listed on the bank statement to spot any differences.

Add or subtract adjustments:

Record any bank fees, interest income, or errors found on the bank statement that are not yet in your accounting records.

Record outstanding items: Account for any outstanding checks or deposits that have not cleared the bank.

Reconcile and verify: After accounting for all differences, ensure the adjusted bank statement balance matches your reconciled internal records.

How do I reconcile a bank statement in Excel?

Use Nanonets to extract transaction data from your bank statement, then export it to Excel. Create a reconciliation template and annotate each column for deposits, withdrawals, bank fees, and checks. Import your ledger data and use Excel’s sorting and filtering tools to match transactions. Apply formulas to calculate differences automatically and use pivot tables to summarize the data. Adjust for any outstanding items and verify that the ending balances match to complete the reconciliation process.